YOUR PROPERTY IS ONE OF YOUR MOST VALUABLE POSSESSIONS AND BIGGEST INVESTMENT

-

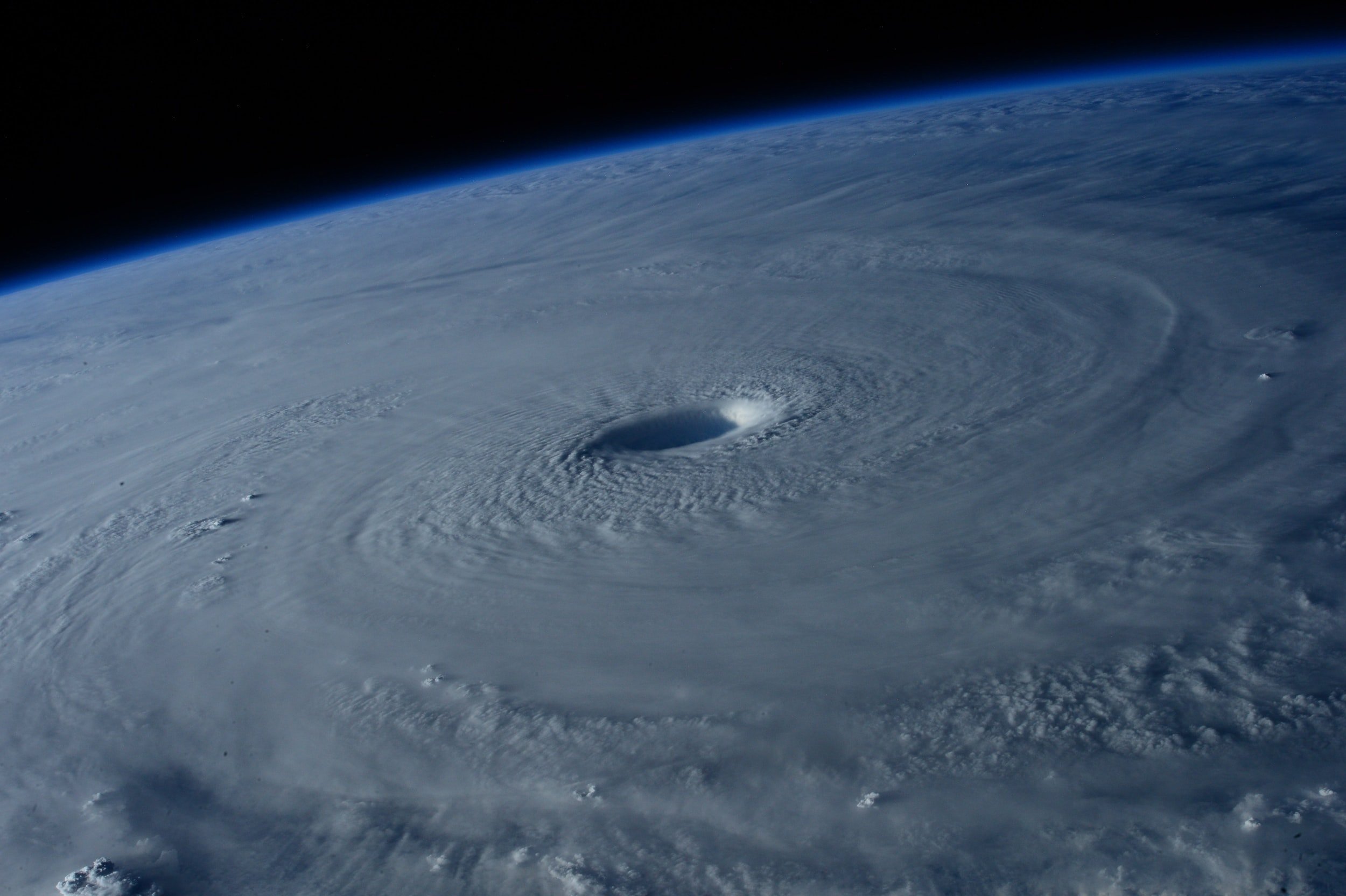

HURRICANE CLAIMS

When your home is devastated by a hurricane, recovering the claim amount from your insurance company can be challenging. Most policies have an increased hurricane deductible, typically a percentage of your home’s maximum coverage amount, which can be a considerable amount compared to the normal windstorm deductible. We will make sure we secure all the necessary repairs for your loss over your hurricane deductible.

Your property is one of your most valuable possessions and your biggest investment. It is important to have the proper work done to the home to restore it back to its pre-loss condition. Hurricanes are common incidences in Florida. Even with the most accurate weather forecasts, storms and hurricanes pose a serious threat to your property.

-

ORDINANCE AND LAW COVERAGE AND WHY IT’S IMPORTANT

We recommend to maintain this coverage. Ordinance and law coverage comes standard with nearly all Florida insurance policies. Most insurance companies will offer you to give up this coverage for a cheaper premium. If you do not have ordinance and law coverage and you suffered a loss there are still options available to you.

Ordinance and Law coverage is an important coverage when it comes to roofing damage. Florida statues states that if you have damage to more than 25% of your roof surface by slope it will warrant a full roof replacement. Simply put, one or more damaged shingles on a slope which makes up more than 25% of your roof may be enough to get your roof fully replaced.

Ordinance and law also covers you for all the latest state and county code requirements and upgrades to keep your home secure for storm season. This includes roofing cement applied to the perimeter of your roof for proper seal, double layering of felt, replacement of rotted sheathing and re-nailing of the decking and more.

-

DUTIES AFTER THE LOSS

Florida Statutes protects homeowners by allowing claims to be filed within 3 years of the loss date. Duties after the loss are requirements set forth in your insurance policy which require you to report the damage to the insurance company within reasonable time, cooperate with their investigation and prevent the property from sustaining further damage.

Many companies are there to help protect your property such as mitigation/restoration companies, roofers and other contractors who can remove damaged property, use proper drying equipment and provide a roof tarp to prevent further water intrusion. The insurance company will pay and reimburse you for all reasonable temporary repairs if coverage is awarded for your loss.

If you paid a contractor or handy man for a repair caused by a covered peril within the last 3 years, and have not filed a claim before, those expenses and any further repairs/replacement may be covered. Lets get started!

If you have filed a claim within the past 5 years we can review and reopen your claim for supplementation. What is supplementation?